Start-Up Cost Calculator

Back to Business Resource Center >

Use our template to find out exactly how much it will cost to start your business, from set-up costs to working capital.

Deposit Checks, Pay Bills, Transfer Money and more with Online and Mobile Banking!

Back to Business Resource Center >

Use our template to find out exactly how much it will cost to start your business, from set-up costs to working capital.

Back to Business Resource Center >

There's a lot of on-going help available for new businesses in Hawaii – including government departments, financial institutions, business associations and non-profit organizations.

Be sure to explore different resources to find what you need to support your business growth at every stage. Ask other business owners for their recommendations on who they have accessed as well.

There are a range of services that you can access, and who you choose depends on your own capabilities and type of business. If possible, choose advisors who have several other clients in your industry because they can often pass along that experience to your benefit. Even better if they specialize in your specific business sector.

Examples include:

A helpful resource for new and existing small business owners, your local Small Business Development Center provides business support.

Key support elements include:

There are several SBDC locations throughout Hawaii. Visit the Hawaii Small Business Development Center website for more details.

Funded by the US Government, SCORE is a non-profit dedicated to helping small businesses by offering free mentoring, workshops, events and content to help you start and grow your business. Other resources include:

Spend some time online to research these resources and discover others. Check out local business organizations and services available to help your new enterprise thrive in Hawaii. Read trusted business publications for a source of growth strategies, business tips and inspiration.

Back to Business Resource Center >

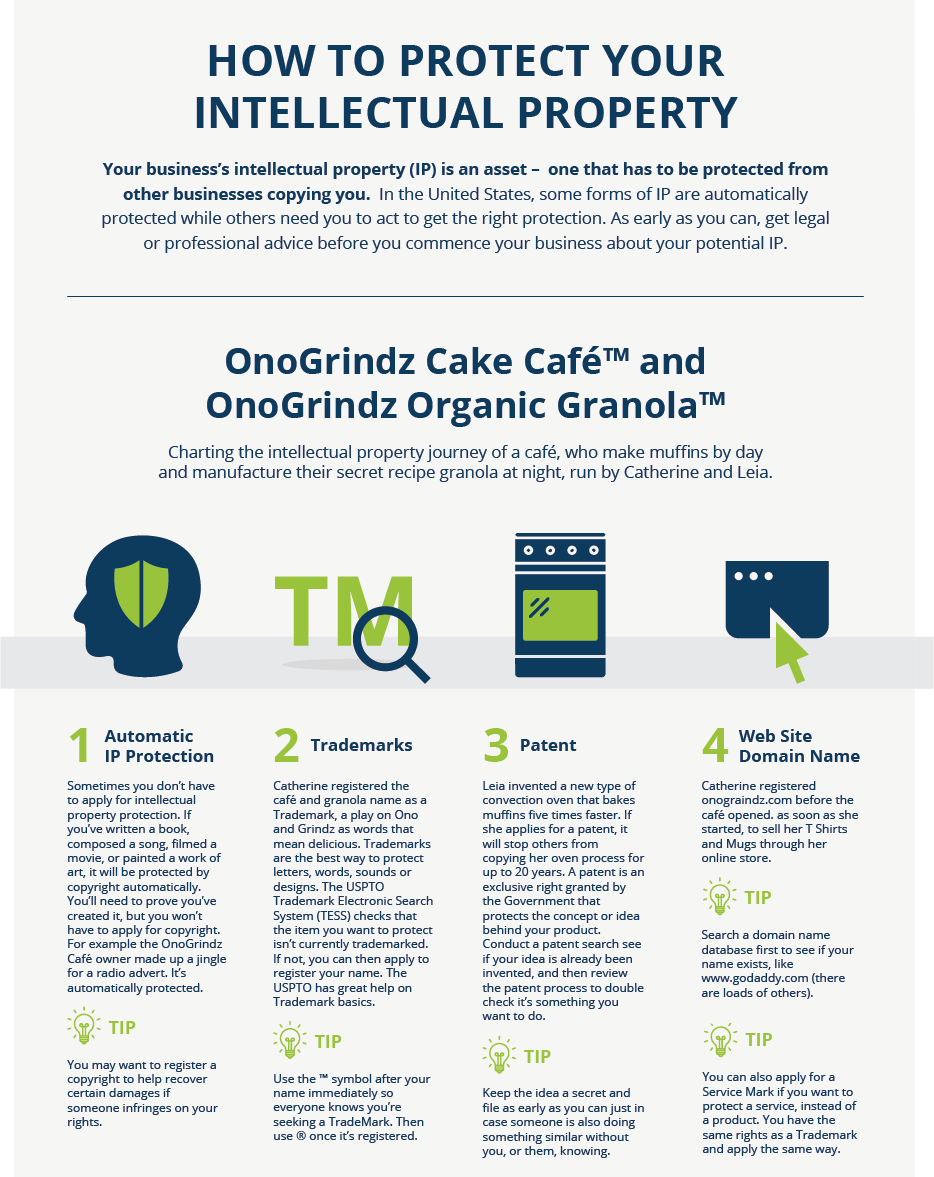

There are a number of risks that you’ll face in business – from employee theft to a competitor using your intellectual property. It’s your responsibility to safeguard your business from anything that may impact your survival and growth.

Like most things in business, prevention is the best cure – a little planning now could save you a significant financial cost in the future. Review the following list of some of the common issues faced by businesses.

To safeguard yourself and your business from being affected by employee misconduct it’s important to take proactive steps to ensure opportunities for fraud are limited. A written policy of accountability and robust cash-handling systems will reduce the risk of theft or fraud.

Customer payments fraud is simply any kind of customer deception that leaves you paying for losses out of pocket.

Back to Business Resource Center >

Once you have a solid business plan, including how much money you need to start your business, one of the next steps is to figure out funding sources to launch your business. Here are ideas to consider to finance start-up costs.

Pulling from personal savings is a common way to invest in your business. You won’t incur any borrowing costs if you can invest some of your own money. You can also consider:

Money from friends and family is a common way of raising the funds you need. But remember, if your business fails, borrowed money from friends or family might sour personal relationships. Be sure to put any financial agreement with a friend or family member down in writing. Clarify when the money is to be repaid, along with any interest.

There could be assets or set-up costs that you can delay paying by borrowing equipment or machinery or working with existing businesses to use any of their spare capacity until your business is big enough to buy your own.

You can borrow money from the bank to get your business started. Bank financing comes in several options. You can take out a loan and pay it back over time, an overdraft facility that lets you dip in and out of debt when you need it, finance equipment or apply for a business credit or debit card for short-term expenses. Talk to an American Savings Bank Business Relationship Manager about our range of business lending solutions.

Before you apply for business financing, it’s important to have all your financial information in hand:

There are several other ways to fund your business, such as outside investors, crowdfunding and government subsidies that can help provide essential funding to launch your business. Here’s some information on each.

Outside Investors

You may find people you know who want to invest in your business. Often called “angel investors,” these people are usually business owners in search of investment opportunities with promising businesses. In return, they usually expect a share in your business, a percentage return on the money they’ve given you or both.

Venture capital companies are professionally run businesses that look to invest in companies they anticipate will be sold to the public, or to a larger company, at a high rate of return. If your business is in a fast-growing industry with a large market potential, you may just catch the eye of an investor.

Crowdfunding

Crowdfunding allows you to profile your business and attract investment—or loans—from a range of different people who wouldn’t normally be eligible to invest in new businesses without a prospectus. You receive investment in your business through a crowdfunding platform hosted online, usually in return for shareholding.

Government grants and subsidies

The government can sometimes provide funds for businesses if you qualify. This includes loans, grants, export assistance and other initiatives. The Hawaii.gov website offers information about different grants and financing options that may be available to your business. The SBA offers loan programs to small business owners. If you are interested in applying, be sure to visit American Savings Bank, as we are an accredited SBA loan provider.

Every dollar you can save when starting your business is one more dollar you won’t have to raise. Unnecessary overhead costs are the last thing you want to deal with, so nonessential expenses should be cut from your budget. Work with your accountant to see where you can save money on start-up expenses.

Back to Business Resource Center >

A business can survive for a short time without sales or profits. But your business needs cash to pay bills and to continue operating. Since cash flow issues can cripple a business, the more warning you have of peaks and troughs, and the more time you have to deal with them.

It may sound obvious, but if you never run out of cash and can pay your bills, you’ll likely never go out of business.

From budgeting to early warning systems, there are many ways to track your money. Consider the following:

Accounting software makes it easier to prepare budgets and forecasts; you can access information coming straight from your bank account. You can also quickly update a monthly cash flow forecast and make “what if” calculations.

If you prepare and update monthly cash flow forecasts showing what cash you expect to come in and what cash will go out, you should know in advance when you might run into problems. Being able to spot any cash flow red flags in advance will give you time to correct any problems and make necessary adjustments.

Decide which profit warning signs hint at a deteriorating cash situation. Comparing short term performance measures to the long-term cash forecast can quickly reveal if sales and profits are going to plan. For example, you could monitor every week or month the following:

Before taking on any large financial commitment, including major new orders or equipment purchases, check that you will have sufficient cash flow to pay. More business may seem attractive, but you don’t want to run out of cash to fund this growth.

Develop red flag systems on less obvious signals to warn you, such as:

There are a number of ways to reduce the chance of your business running out of funds. The most obvious tactic is to have enough cash reserves to be able to ride out any fluctuation or downturn. Every business should always be looking to implement the following:

When negotiating contracts with customers, make generating cash flow one of your primary objectives by asking for deposits or progress payments. Staged payments improve your cash flow and protect you from total loss if a customer fails to pay.

Improve your sales and profit margins by invoicing on the same day. Consider collecting payments using mobile payment options immediately after any work is complete. With larger customers, ensure you have purchase order numbers in advance so you can enter the customer’s payment cycle faster. If appropriate, follow up and confirm the invoice details and due date.

Efficient credit control systems speed up cash collection and reduce bad debt, saving time and showing lenders and investors that you run your business professionally. Consider debt collection agencies or lawyers specializing in debt collection can be effective in difficult credit situations.

Regularly ask suppliers to renegotiate. Consider carefully when purchasing capital equipment or any other large-scale purchases. Ask yourself whether you really need the equipment, or if it can be borrowed, leased or rented instead.

Good stock control can release substantial sums of money as it prevents you from having large amounts of money tied up in inventory or raw materials. Use inventory software to hold just enough stock to service customers on an on-going basis.

It is important to be aware that even if you are profitable and sales are increasing, a lack of cash flow can still significantly harm your business. Create contingency plans, including how much additional working capital you’ll need to fund any increase in sales and the associated costs of job growth. Have cash in reserve or a plan to access capital to remain in business. Finally, monitor that you’re not withdrawing too much capital so that it puts your business at risk.

Markets are dynamic and constantly evolving, no matter how excellent your current products or services. Therefore, it’s useful to regularly redevelop, replace, upgrade or update your products and services to continue growing your business. Here are some practical methods to uncover a potential new product or service in your business.

To find new product or service ideas try the following:

Finally, contact your customers and ask them what else they need, what are their issues and problems that you can help to solve.

While a good idea has no guarantee of success, a bad idea will most certainly fail. Here are some signs your new idea could work:

Since product development involves time, labor and finance, it’s important to plan carefully in advance. Minimize your risk by applying some sound management techniques to your planning process. Create a team with the skills needed to make the project a success and choose a team leader.

Every new product needs a champion to lead the team. Incorporate the following:

Once a prototype of the new product has been produced, or a new service decided on, it needs to be tested. A soft launch done locally with a few customers is a smart way to test the waters and gather feedback. You can find out what customers think and tweak your new idea, if needed.

Testing will reduce the major risks early so you can decide if it’s worth the potential reward. Minimize the risk by:

Successful businesses are those that are continually looking for ways to innovate. This is an essential component for achieving growth. Whether it’s a new product or service, or one you’ve come up with that’s designed to complement existing ones, make sure you consider all the above carefully, as this will help maximize your chances of success.

Back to Business Resource Center >

Increasing sales might make more profit for your business but consider increasing profit margins –especially if there is limited opportunity to increase sales.

Growing your business can be achieved by growing profit rather than sales.

Increasing the price of your goods or services seems the obvious answer when trying to improve margins. And it is. Nothing will improve your margins more than a price increase (with the understanding a price increase could cause a drop in sales if you’re over-priced).

However a price increase will always improve your margin. Try:

If you have price sensitive customers, then consider the impact on sales that a price increase may have.

There will always be a threshold where customers will switch for a lower price regardless of how great your business is, especially for products and services where customers have a fair idea of the cost.

If you do sell items that are price sensitive, keep your major products or services at competitive prices. Instead, think about increasing margins on supplementary products or services where customers are either not so familiar with the price or don’t compare you with the competition.

The other main way you can improve your margins is by lowering the cost of supply – finding ways to pay less for any of the costs associated with bringing your products or services to consumers.

To achieve lower costs, consider:

Concentrate on the products or services you sell that have the biggest margins – by selling more of these items, your business will gain more profit. Train your employees to be aware of which items have the biggest margin and are therefore best to sell if the customer is unsure. If you need to, allocate incentives or bonuses for selling high-margin items.

Likewise, begin to phase out goods that have low margins. If you’re selling plenty of them but not making much profit, it might be best to use that space or time for something more profitable.

Other options for focusing on larger margins include:

Remember the 80/20 rule outlines that 80% of your profits comes from 20% of your goods or services. Make sure they are the high-margin products.

Change the customers you are targeting to ones who will spend more money or who are less price resistant. They may be quite happy to pay a higher price for what you offer.

Consider only doing business with those customers that pay on time, or in cash, or don’t always want a discount. By not having to wait for your money, you will enjoy higher margins by either paying less interest on any financing or receiving interest on spare cash.

Are there any clients that cost less to service (such as closer to your location or don’t require on-going support)? Having more of these customers will lower your overall costs and, therefore, increase your margins.

You could open new locations or target new regions where customers are willing to pay a higher price. If you focus on local consumers who are price sensitive, can you find commercial or government customers who may be prepared to pay more for what you do?

Some businesses are able to reduce their fixed overheads, such as replacing salaried staff with part-time or contracted workers. In addition:

Realizing higher margins removes some pressure from sales because it means you can sell fewer products and services, or the same amount, and return a higher profit. Get in the habit of regularly reviewing your margins to make sure they haven’t changed due to creeping input costs or sales discounts. Repeat these strategies often to keep enjoying healthy margins in your business.

Back to Business Resource Center >

Keep in mind that a profit increase doesn’t always have to focus on driving sales. Often improving a number of things a little better has more impact than making one large change.

Consider implementing the following tactics at the same time to achieve an accumulative effect on your profit.

If you can increase or decrease ten percent of your business that links to profit (or even five percent), then possibly customers will either not notice (unless you are in a very price sensitive market), or be fine with the changes.

Increase prices

Raising prices can lift your profit, but take care to check with your customers to see how they’d react to a price increase. If such a change lowers your demand and you lose customers, your profit margin may go up (as you’re charging more) but your overall profit may drop. To reduce a drop in sales while increasing prices try:

Always monitor the effect of a price rise to detect any unhappy customers.

Increase revenue

A simple increase in sales (without discounting) should increase your profit. Some ideas to help you increase turnover include:

Reduce costs

Identify the steps you can take to minimize your direct costs, such as:

Divide your customers into four categories and put different effort and resources into selling to them depending on their value. For example customers that have a:

Take into account any possible effects of increasing profits before making decisions. For example, a low-profit product might be the one that brings other business from a major, highly profitable customer.

Focusing staff on profitability can have also a dramatic impact if they are aware that small savings can benefit everyone. Develop incentives if they assist with:

Operating efficiently is essential to a sustainable, profitable business. From negotiating better terms with suppliers to nurturing your most profitable customers, your efforts can pay off.

Consider changing a number of things in your business all at once, to gain that cumulative effect on your profit.

Get started today for a more profitable bottom line.